Learn the benefits of managing debt plus tips to improving one’s credit score.

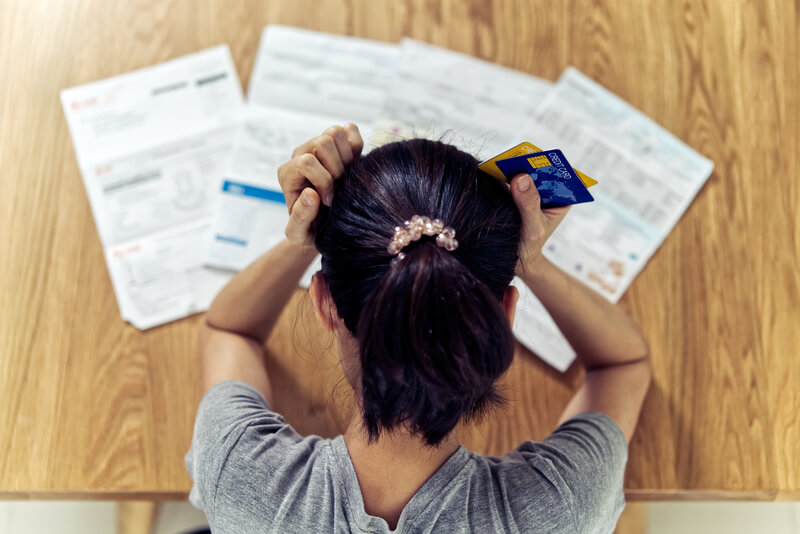

Most Americans carry debt

Many Americans make New Year resolutions to improve health and wealth. These highly achievable goals involve adopting better habits. When it comes to money, many Americans fail to spend, budget, and save wisely. The inability to repay borrowed money within the required timeframe is one consequence of poor money management. Consumer credit report company, Experian, shares that average American debt reached $105,755 in June 2025. Here is their breakdown by generation:

- Generation Zers: $34,328

- Millennials: $132,280

- Generation X: $158,105

- Baby Boomers: $92,619

- Silent Generation: $38,460

What does this all mean?

Based on their anonymized data, Experian shares that many American consumers have at least one type of debt, with older generations borrowing from multiple sources. They explain, “So while some consumers – notably Gen Zers who are just starting to borrow – may only have a credit card or two to their name, older consumers are likely to be carrying a mix of credit types over time.” And, as consumer costs have increased over the last few years, likely to include interest rates and the cost of what’s being financed, many consumers end up paying more than they bargained for. This can stretch some people’s finances thin.

Carrying heavy debt

Carrying debt, particularly large debt loads, is generally not beneficial. This can make it harder to make monthly payments, save for the future, qualify for additional credit, etc. Having heavy debt can result in serious money-related fear and anxiety. Per Health.com, “Debt has been shown to increase the risk of anxiety, depression, and suicidal thoughts. Stress from financial burdens can also worsen existing mental health conditions.” Finding fresh ways to recover from or stay out of debt is worthwhile to overall wellbeing. While digging oneself out of a financial hole is likely challenging, creating a plan and taking steps to achieving financial fitness make debt reduction doable. Consider calling your credit card company to request a reduction in interest rate. If you can’t handle your finances yourself, get consumer counseling to help you get back on track – but choose a reputable agency and be mindful of those which charge fees.

Snowballing debt

Debt essentially happens when people spend and borrow more than they bring in. When the pattern continues, debt accumulates. High interest rates or fees for credit cards, car payments, the mortgage, and other bills can worsen debt. Debt that is hard to repay indicates that people are living outside of their means. Two main ways to avoid or lower debt are: 1) Increasing earnings and income and 2) Decreasing wasteful spending.

Here are some other helpful financial tips:

- Make a commitment to do better. Being serious about improving finances puts people on the right path to successfully make responsible decisions and hit financial goals. Being accountable for one’s finances pushes people to be deliberate about their actions or face the consequences.

- Know where you stand. Track your income and expenses to see what’s coming in and where your money is going. This makes budgeting and saving possible, designating an all-important purpose for your money while discouraging unnecessary spending.

- Create financial goals. Make a list of short and long-term financial goals and create actionable plans with timelines. For example, save for a home down payment now while also contributing to retirement.

- Budget wisely. Budgeting lets you manage your money by deciding where it goes. Building wealth is a vital part of budgeting; offering the freedom to save and invest, make large purchases while avoiding debt, and prepare for the unexpected.

- Cut wasteful spending. Wasteful spending can lead people to struggle financially. Questionable spending and overextending oneself financially can harm credit and negatively impact one’s ability to borrow money or pay down debt. Reducing unnecessary expenses means focusing on essential needs instead of desires.

Tips for cutting wasteful spending:

Look through recent bank statements and focus on places where you’re spending money unnecessarily. Two examples include dining out and paying for subscriptions.

- Dining out. Eating out is an expensive activity. Not only do restaurants pass along their overhead costs, but customers also pay additional tips for service. Ordering alcohol and dessert can significantly increase the bottom line. Instead, cook at home and reserve dining out for special occasions only.

- Subscriptions. People often lose track of the money they are spending on subscription services they don’t use, particularly those which automatically renew. This may include things like television subscription streaming services, shopping clubs, gym memberships and more.

Good practice

People should continually review their spending habits, manage debt, and monitor their credit score.

Credit score equals a numerical summary of your credit health

Credit scores are three-digit numbers (typically between 300 – 850) that are generated based on information in one’s credit report. Lenders use credit scores to predict how likely a person is to repay borrowed money. The score affects whether lenders will do business with you. A low score indicates “poor” credit – meaning that a person is a high financial risk. A high score means a person has “good” credit and is less of a financial risk. People with poor credit have a harder time getting loans, whereas people with good credit are welcome to do business most places. Since FICO scores are widely used by most lenders, let’s review what the numbers mean.

Key score ranges (FICO):

800-850 = Excellent

740-799 = Very good

670-739 = Good

580 -669 = Fair

300-579 = Poor

Some good news!

The good news is that people can control the general direction of their credit score through consistent and responsible financial habits. Some practices that can positively influence credit scores include:

- Paying bills on time. Payment history is a crucial factor (35%) in determining credit scores. Lenders look for people with a history of making timely payments. Paying bills late and even having small delinquencies can negatively impact credit scores. Paying bills late can also trigger late fees and make it harder to pay back debt.

- Avoiding bankruptcy or collections. People who have declared bankruptcy or have had accounts put in collections will be negatively impacted. Per Frego & Associates, “Bankruptcy creates a public record that remains on your credit report for several years. This record serves as a red flag for future lenders and can make it challenging to access credit or obtain favorable terms.”

- Keeping a low credit utilization ratio. Scoring systems generally look at the ratio of debt to credit limit. Credit debt refers to the amount of money you owe to creditors and credit limit is the maximum amount of money creditors are willing to give. If the amount owed is close to one’s limit, this will likely negatively impact credit score. It’s generally better to have lower amounts of debt as compared to one’s credit limit.

- Avoiding too many credit inquiries. Too many credit inquiries can temporarily harm one’s credit score and make it harder to be approved for credit. Per FNBO.com, “Having multiple hard inquiries in a short amount of time could negatively impact your credit score because it could mean you have too many new accounts on your report. This is often an indication to a third party that a borrower is having trouble paying bills or could be taking on too much new debt.”

- Building a mix of credit over time. Good credit builds with time. Having the right amount of existing credit and the right type of cards matters. This means having a mix of credit cards and loans (revolving and installment accounts) that are paid back responsibly.

- Understanding consequences of closing out old cards. This action can give your credit score a hit by reducing your total available credit and potentially increasing your utilization ratio and hurting your score.Some folks might consider closing cards that they don’t plan to use anytime soon. But wait, understand that choosing to close a card that’s been open for several years with a lengthy history could harm credit. Uncertain? Talk with your financial planner and/or do your homework to understand potential consequences of closing out credit.

To learn more about what affects your credit score and managing debt, visit www.experian.com

Disclosure: This article is purely informational and is not intended as a substitute for professional financial advice.

[adrotate banner=”1094″]

If you have a spending problem, you’ll eventually have a debt problem. Unfortunately the cost of living has many facets that we cannot control. For example, inflation or as I call it a government reset where everything commerce costs more because our money is worth less and therefore it takes more money to buy the same items. Governments explanation is ambiguous because it’s not just one line item that goes up but literally everything. So spending becomes discretionary, it’s now what can I do without? Buying slightly cheaper store brand groceries, putting off repairs or putting it on plastic. We spend our way into debt and for the most of us income will never keep up the cost of living.

Been there, done that. This is good advice. The debt management company that helped me work with my creditors was Apprisen. Their fee was minimal and we’ll worth it.

My credit cards are paid in full every month, the only debt I have is a very manageable car payment, my credit score is now 832 and I live very comfortably.