A fully implemented Affordable Care Act would “bend the cost curve” in health care, “moving the health care system toward higher quality and more efficient care,” according to a White House statement in 2013.

Many people now agree that didn’t happen.

“We pay more than any other country in the world for worse health care,” Sen. Elissa Slotkin (D-Mich.) said while campaigning for office in 2024.

“Families pay more, get less, and we’re left with few choices,” Rep. Mike Lawler (R-N.Y.) testified in a December 2025 committee hearing.

A combined 70 percent of Americans believe the U.S. health care system is either in crisis or has major problems, according to a 2025 Gallup poll.

Health insurance premiums have more than doubled since the major provisions of the Affordable Care Act, commonly known as Obamacare, began in 2014, rising twice as fast as inflation. And satisfaction with the cost of health care registered a record low in 2025, at 16 percent.

How did that happen?

Consumers have said that insurance companies are responsible. Insurers shift the blame to hospitals and pharmaceutical companies. Pharmaceutical companies say pharmacy benefit managers are at fault. Political parties blame each other.

Some independent observers agree that the rise in premiums, especially recently, is largely driven by external forces, including the increased use of expensive medications, rising labor costs, and inflation, which reached a 40-year high in 2022.

Others see a more basic cause, one with roots in the Affordable Care Act. Some of the same policies that make Obamacare popular with consumers are actually cracks in its foundation, these observers say. Those policies all but guaranteed premium increases, especially in the program’s early years.

Here are the key provisions of Obamacare, which some experts say undermined its success.

Foundations of Obamacare

The Affordable Care Act made profound changes in the health insurance industry. One of the changes required insurance companies to issue health insurance in the individual and small-group markets to any applicant, regardless of preexisting illness.

Americans generally like that idea. More than two-thirds of people say that provision is very important, according to polling by health care research group KFF. That includes 54 percent of Republicans, 66 percent of independents, and 79 percent of Democrats.

Known as guaranteed issue, this was one of four foundational provisions built into Obamacare to make health insurance available to more Americans.

The second foundation was community rating, which required insurers to rate, or price, their plans based on the demographic profile of a community, with only limited increases based on age and tobacco use. According to this provision, premiums for people of the same age group in the same geographic area are pretty much the same.

The third foundation was the requirement that certain essential health benefits be included in every plan, except for catastrophic health plans. This ensured that consumers would get real value for their money and not be surprised to find that services such as emergency room visits and maternity care were not covered.

The Department of Health and Human Services eventually decided on 10 essential health benefits.

The final foundation was the individual mandate. This required most adults to either buy health insurance or pay a fine. The point was to keep overall costs down by ensuring that young, healthy people, who would likely incur fewer charges, would stay in the market. The fine was $95 per adult in 2014 and rose to $695 by 2016.

Although some of these provisions were popular with consumers, they increased both cost and risk for health insurers. And although the new rules made insurance premiums lower for some customers, prices went up for some others.

And the new rules applied to all new plans for individual and small-group insurance sold in the United States, guaranteeing a shift in the entire market, not just the Obamacare exchanges.

Higher Cost, Increased Risk

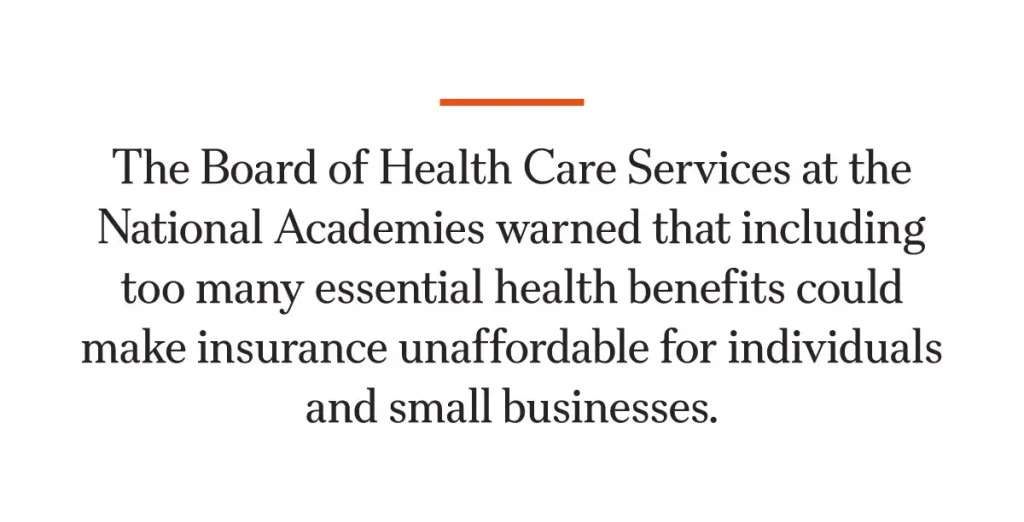

As the Affordable Care Act was being considered and implemented, stakeholders warned that these sweeping changes could make insurance more expensive. At a minimum, they said, the requirement that plans cover a suite of essential health benefits could raise premiums.

The Board of Health Care Services at the National Academies warned that including too many essential health benefits could make insurance unaffordable for individuals and small businesses.

“If this occurs, the principal reason for the [Affordable Care Act]—enabling people to purchase health insurance and thus covering more of the population—will not be met,” the board wrote in 2012.

Insurers were also wary. America’s Health Insurance Plans, an industry trade group, told regulators in a 2012 letter that the choice of essential health benefits would have “far-reaching implications” on the affordability of health insurance.

Increased risk was also a concern.

Insurers speculated on the legality of the individual mandate and warned that Obamacare wouldn’t be viable without it.

“The insurance market reforms cannot function as Congress intended without the mandate and therefore should be struck down if the mandate is held to be unconstitutional,” the insurance trade group argued in a brief filed with the Blue Cross Blue Shield Association.

The old risk management strategy of medical underwriting—pricing premiums based on the underlying health risks of an individual or members of a small group—was no longer an option.

Community pricing would reduce premiums for people with preexisting conditions or other health risks. But premiums would increase for younger and healthier people. Some observers feared that younger people might stay out of the market, then buy health insurance only when they became ill.

If that happened, it would throw off the risk predictions insurers had made, leaving them with an older, sicker population to cover. In the insurance business, this situation is known as adverse selection.

Timothy Jost of Washington and Lee University School of Law, in a 2010 report for The Commonwealth Fund, called that possibility “the greatest threat facing exchanges.”

Michael F. Cannon, a health policy expert at the Cato Institute, in 2010 saw the potential for an “adverse-selection death spiral.”

Risk Mitigation

The Affordable Care Act acknowledged the increased risk for insurers and included three provisions to keep premium prices stable.

First, the law included a risk adjustment. This was meant to protect health plans that wound up ensuring an exceptionally high-risk group of people. Plans that wound up with a lower-than-average risk group would make a payment to plans having a higher-than-average risk group.

Second, the law included a reinsurance program. This was to help plans deal with unexpectedly high medical costs for an individual enrollee. All insurers paid into a reinsurance pool. At the end of the year, each could submit a claim for individual enrollee costs that exceeded a certain threshold. This program, which was intended to be temporary, ran from 2014 through 2016.

Third, the law created risk corridors. This was to help health plans that had total claim payments exceeding the predicted amount. Plans that had lower-than-expected claim totals would pay into a fund. The fund would make payments to plans with claim costs higher than their target amount. This program was also intended to be temporary and ran from 2014 through 2016.

The Spiral Begins

The first several years of Obamacare had lower-than-expected enrollment, higher-than-anticipated costs, and diminishing choice in the marketplace.

Enrollment was significantly lower than expected in the early years, which observers had warned could be a sign of adverse selection.

After a shaky start due to glitches in the online marketplaces, enrollment in 2014 actually exceeded the modest Congressional Budget Office forecast.

Yet the overall market grew by just 4.2 million that year, as many of the 8 million Obamacare enrollees were people who had moved over from the commercial market, according to a report by Amanda E. Kowalski of Yale University.

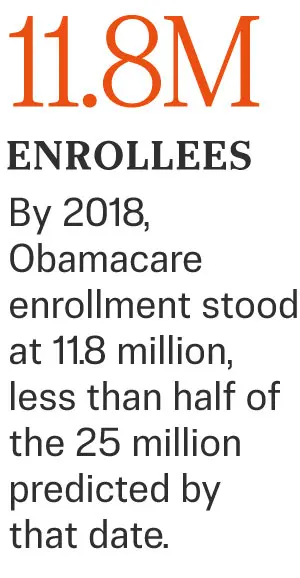

By 2018, Obamacare enrollment stood at 11.8 million, nearly 1 million less than in 2016 and less than half of the 25 million predicted by that date.

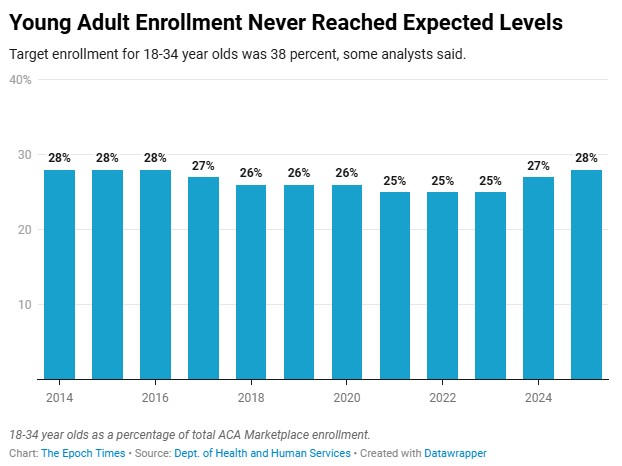

Data suggest that many of the missing enrollees were young adults.

Obamacare needed an enrollment mix that included 38 percent young adults to avoid a “death spiral,” the Cato Institute reported in early 2014.

At the close of its first enrollment period in 2014, Obamacare had an enrollment pool that was just 28 percent young adults aged 18–34. A Commonwealth Fund report indicated that people whose premiums increased had been slightly less likely to buy insurance in 2014. Young adults would have been among those whose rates went up.

The individual mandate, which aimed to offset this factor, faced court challenges beginning in 2010. Although it was not ultimately ruled unconstitutional, Congress set the penalty for noncompliance at $0 in 2017, effectively ending the federal mandate.

Enrollee age was not the only indicator of adverse enrollment, Kowalski reported. Her analysis of cost data concluded that marketplaces in at least 16 states experienced adverse enrollment in 2014.

Data indicate that the cost of insuring Obamacare enrollees exceeded expected levels in the early years.

The reinsurance program had obligations exceeding income by nearly $10 billion over three years.

The risk corridors program fared no better. Income was insufficient to meet obligations in 2014, so all 2015 income and at least a part of 2016 income was used to pay off the 2014 shortfall.

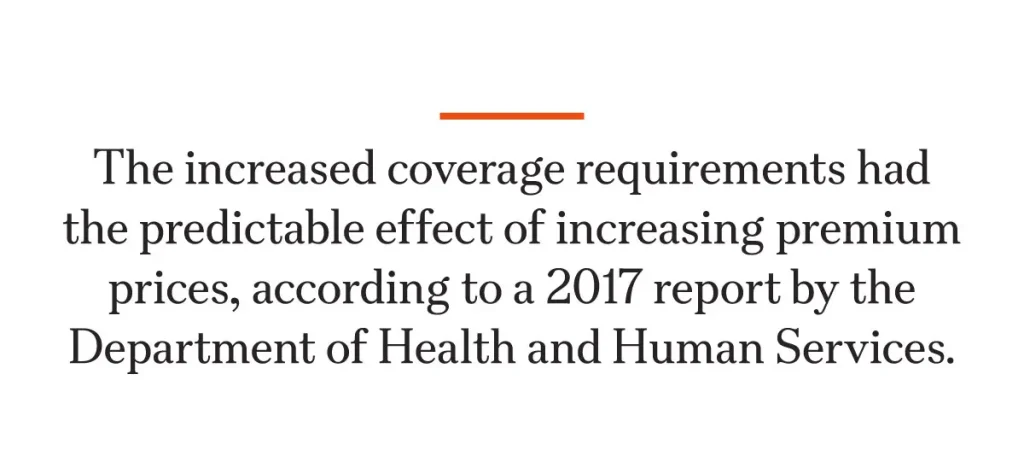

The increased coverage requirements had the predictable effect of increasing premium prices, according to a 2017 report by the Department of Health and Human Services.

“In most states these regulations increased insurance coverage requirements and would be expected, on average, to increase the price of [Affordable Care Act]-compliant plans relative to pre-[Affordable Care Act] plans all else equal,” the report reads.

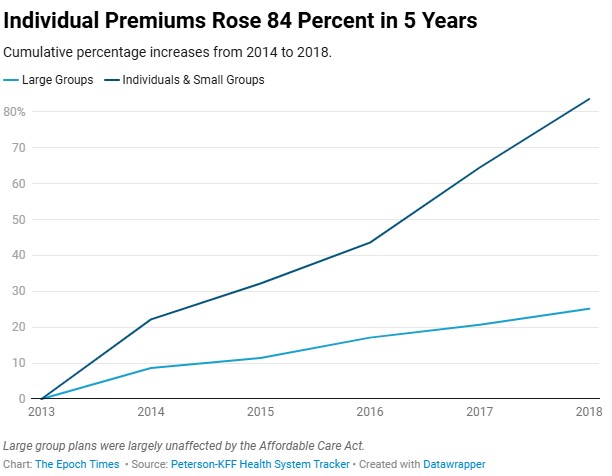

Premiums increased by 22 percent in the first year and a total of 84 percent by 2018.

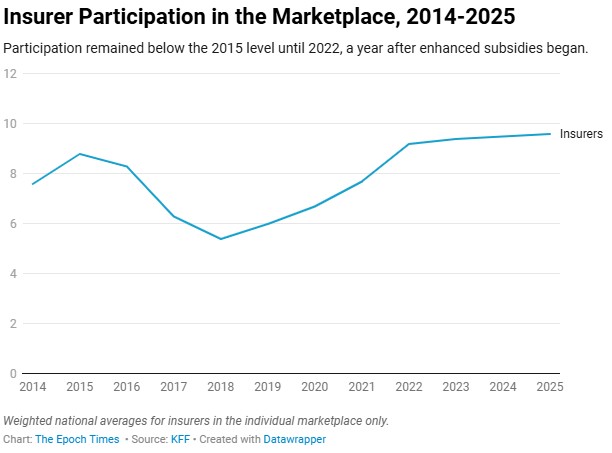

Insurers began to leave the marketplace. In 2015, an average of 8.8 insurers in each state participated in Obamacare, according to KFF. By 2018, that number had dropped to less than six.

The COVID Years and Beyond

In the middle years of Obamacare, enrollment decreased, then plateaued after reaching a high of 12.7 million in 2016. Premiums decreased somewhat, too, dropping by about 9 percent over four years from their high point in 2018. And insurer participation ticked up slightly in 2019.

Then came COVID-19 and the enhanced premium subsidies created by Congress in 2021.

Those enhanced subsidies, which expired in 2025, provided financial help to Americans with higher incomes and further lowered the cost of Obamacare for low-income people. Enrollment more than doubled, reaching an all-time high of 24.3 million in 2025.

Yet as enrollment spiraled upward, so did premiums. Prices reached a new high in 2025, averaging $497 per month for a 40-year-old enrolled in the most popular plan.

What didn’t change dramatically was the age profile of enrollees. Although some young adults entered the market in the era of enhanced subsidies, their numbers never exceeded the 2014 rate of 28 percent.

And despite a rise in the number of insurers doing business in Obamacare, some of the largest companies have said that they find it unprofitable.

David Joyner, CEO of CVS Health, testifying before Congress on Jan. 22, said its costs exceeded income in the Obamacare marketplaces in 2025, and Gail Boudreaux, CEO of Elevance Health—the parent company of Anthem—said it did not turn a profit from Obamacare in 2025.

David Cordani of The Cigna Group said, “We lost money in the exchange all but two years since 2014.”

Lawrence Wilson is a Senior Reporter for The Epoch Times and covers healthcare and politics.

Reprinted with Permission from The Epoch Times – By Lawrence Wilson

The opinions expressed by columnists are their own and do not necessarily represent the views of AMAC or AMAC Action.

Bottom Line — Obamacare was one of the biggest scams that the Democrats forced unto the people with many lies. It needs to be gutted and shredded. The Democrats should be forced to repay the taxpayer for such a waste but that won’t happen. The scamming continues as Virginia Democrats have unleashed many ridiculous taxes on its citizens and visitors.

Make the Government employees and Congressmen all have the same medical insurance plans available as the “regular folks” and believe me, they will change their minds on how to manage this mess.

A very maybe too informative article, describing what has happened to the medical insurance for all of us. When low risk are forced to pay for the high risk, this is just wrong on all counts. I like the President’s plan, let the people shop for their own coverage, like they do for home and auto insurance. Of course there’d be no kick back for those making the laws, just saying.

It is Obamacare, no explanation necessary, what else could it possibly be than that which it is. Did anyone expected it to be a success, surely not one person could be that dense, he showed us all what his capabilities are prior.

Obama was a cheater and a liar. He admitted everything he said about keeping your health care provider and keeping your plan were lies. But that’s redundancy he’s a Democrat so we know he’s a liar. I remember when they were trying to calculate the cost and they counted assets twice as somebody said you can’t do that and it said yes we can it’s the only way we can make it work. The whole thing was a fraud. And that moron supreme Court Justice gave it to us he’s the one that decided that the federal government could mandate that you have to buy it. He could have shut the whole thing off they had some dirt on him that was unbelievable we still don’t know what it was. Everything the Democrats do is wrong every decision they make is wrong they do nothing but lie and cheat they are the party of Satan. Give me a minute and I’ll tell you what I really think of them

Total failure. Democrats should face the blame for this mess. But, the reality of it is, they don’t give a damn about you or I.

Unfortunately, most insurance plans are basically catastrophic insurance. Premiums are high as is the deductible. You have to pay thousands of dollars before the insurance company pays, usually 80/20. Obamacare is a ripoff. No wonder Nancy Pelosi said that in order to read what’s in the bill you had to pass it first…..

It will take several more decades before the stink of Obamacare dissipates. What a disaster.

one item not discussed is the cost of malpractice insurance and the high payoffs for lawyers. Limits on awards are needed. In some states usually red there are limits set. A few years ago doctors were choosing states like Texas for their practices. Every cost to a hospital, doctor any health care provider needs to be addressed.

This is article is very thorough and informative packed with a boatload/ rabbit hole of facts and stats to get lost in.

The thing is that the Affordable Care Act started off way back in 1992/ 1993 as the Health Security Act which wasn’t really an act at that point because it was rejected by the very political party who was trying to get it passed.

Long story short, once you’ve researched it for yourself, only then will it become clear that it was all designed from the beginning to fail for the very people it was supposed to provide protection for and enrich those who wrote it and keep it going for as long as possible.

Find out who was the original author for the mess that was written roughly 33 or 34 years ago and you’ll start to understand why they want this grift to continue on without end.

What the ACA fails to do is address the underlying cost factor that makes those premiums btoh unaffordable and healthcare coverage available at reasonable level costs. NYS is already an expensive state, and healthcare costs in NYS are one of the highest in the nation because of the fact that those who py the premiums have the burden to cover the extra cost for the health insurers who are covering the healthcare services of the higher number of individuals in NYSm who get the “free healthcare” coverage under the Medicaid expansion. It created a massive hole in the number of individuals who don’t qualify for the “free healthcare”coverage because their income is barely over the maximum income–that income level is mere dollars over the property income line– and their income is not the supposed “dream income average of $80,000/year either. This created a donut hole in the population who are uninsured with a healthcare policy, plus can’t afford to get the healthcare service because the out of pocket cost are so high. These same uninsured individuals are members of the working class, who pay taxes in there earnings that provides the “free healthcare coverage” to those who deliberately work in cash only positions to not have reportable income that will force them to pay for the healthcare they get for “free”. The system encourages too many people to not earn enough recorded income (46% of the population). Being a member if the population whose earnings were always recorded on record. I did not appreciate my healthcare costs quadrupling once the ACA started the point that I had for almost 5-6 years (from age 60-65) no healthcare coverage until I qualified by age to get Medicare, and I pay that Medicare premium (taken directly out of my Social Security benefit) and all out of pocket costs because my social security benefit earnings is considered too high to qualify for the aid of Medicaid to cover the out of pocket costs, which are rising higher and higher, plus have to pay taxes on m social security earnings

ACA was a disaster from day one. It never caught on till COVID and the taxpayers paid subsidies to those who couldn’t afford the premiums. It still was the people thru tax money that paid for it. Just so ACA could stay as a crowning glory to Obama’s regime. It was not a glorious law or policy. It was written full of fraud and angled for the insurance companies to get around paying for the benefits. And speculation that young people would enroll to pay for the elderly. They put a penalty if they didn’t join. No they should have made it mandatory for everyone to join ACA. And not make a plan as to what was insured. Everything should be covered. But what happened. Medicare patients were not covered under this law. Many drs and dentists stopped taking Medicare altogether. This you can keep your Dr with ACA wasn’t true. This bill was written for the insurance companies and big Pharma. The citizens are getting sicker and the insurance company got richer. There should be an insurance bill where everyone has to insure themselves and all insurance companies should follow the same guidelines. Now some insurance companies will pay for certain benefits while others deny them. Or copays are lower by some and higher by others. Or change from year to year. Raising the premiums and lowering benefits has to be addressed under a new health care bill. Now it is a crap shoot. Which company is the best for my family. Nobody knows. There should not be competition. Benefits and premiums set by the bill. And insurance company have to abide by those guidelines. Now it is a competition and after the first year they change everything and once again you have to go shop around which company gives you the best deal. It’s a for profit business but the democrats only thought of the business end and forgot about the people. Pelosi got rich by passing this bill by saying “we have to pass this bill to know what’s in it”. Boy did we find out. Billions of dollars for the insurance industry, death for the citizens. Because no one can afford to get ill in this country. The insurance company pay nothing or deny your claims. A few days in the hospital breaks he most affluent American.

No one ever READ THE ENTIRE DOCUMENT. “We need to pass the bill to see what is in it”….nanner pelosi in her INFAMOUS MIDNIGHT TIRADE TO PASS THE POS bill.With NO GOPvotes—this is ALL ON THE dem/lib/commie/socialist/fake news arse holies and their desire to destroy America from within. Their goal was to take over the healthcare industry and have the government take it over. What a crock of ……….

A functioning congress might take the data as proof of failed healthcare plan. Unfortunately our congress is focused on itself and they don’t use Obamacare. When did we think this would work?

Obama, the name screams corruption and lies. He was forced upon us by the “uniparty” with his proven fake birth certificate and the woman who created it conveniently died in a plane crash – she was the only one of the many who died, so she could not testify – sound familiar? Like a Clinton took care of the problem? Anyway, if you remember, the insurance companies had a fit when the ACA was first proposed. Then, later, we did not hear a peep. Now we know why. The Dems got kick back money to make the ins companies wealthy with changes to the ACA. One can only hope that Trump is collecting evidence and will bring down the hammer on all the corrupt liars in our government and beyond.

Obama Care was definitely a farce! My husband had to have tests because of his breathing problems – you would not believe what the hospital required him to have to tell him he had COPD and Emphysima! The bills we now have are astronomical!!! I guess they will have to go to collection, because we live on my SS and he is my FULLTIME Caregiver, with no extra $ for him!!! JUST WHAT I CAN AFFORD IN NORMAL LIVING EXPENSES!! OUR CREDIT CARDS ARE MORE THAN THEY HAVE EVER BEEN…..

Yes obama care cause rise in health care cost BUTT !! How much do doctors charge ( sick ). What your hourly wage.

Are they doctors for the patients or the almighty evil $$$ . Mostly a bunch of quacks practicing quack quackery. Almighty dollar make not a doctor.

tell em ewe charge to damn much

Way the Dems planned O Care??

Why is anyone shocked by the rising Medical costs. Obama said “Prices will necessarily Skyrocket”. Remember the goal was to destroy the then and now Medical System and replace it with a single payer system. The Democrats have done it, Pelosi said and got passed, the Democrats Bill ACA “We have to pass this Bill to see what’s in it”. What our Politicians did to health care, and Education have SkyRocketed costs well beyond what people can afford. College and Hospitalization used to be affordable now you have to sell your first born child for the priviledge of taking out loans to pay them off.

It’s all intentional. It was never meant to succeed. Obamacare is one of the left’s biggest dirty tricks on citizens.Many on the left spoke the truth out loud, but people didn’t listen. Obamacare was a step-up interim plan intended to fail and push Americans into a national health care system, the likes of which are in UK, Canada, and much of Europe. “Free” health care for all! Which turns out to be mediocre health care for all, and throws the elderly and those with severe medical issues under the bus eventually. Decisions are made based partially on age and life expectatio as to what medical care you’re eligible for, and which (priced) drugs you can be prescribed. In other words, if you’re too old or too sick to be expected to live.long enough to make the financial investment for you to have a surgery or treatment worth the system paying for it, in their opinion, then you’re denied under those systems. I know it works this way because I personally knew two people it happened to, one in Germany denied removal of what doctors called an operable cancerous tumor with a good success rate, because he was over 55 years old at the time (denial stating his statistical life expectancy due to his age as a reason); and in Canada a woman who was denied a rather common, but life-saving heart surgery because she was 62 years old. In both countries, they were not allowed to have the surgeries even if they paid for it themselves! The latter, thankfully, was well enough off that she came to the US and paid to have the surgery at Cleveland Clinic, and is still alive some 15 years later. The former just accepted the decision and his fate, and he died from the cancer. There is a reason countries like Canada and some others push euthanasia on people. Let’s not become Canada — or even the UK, where waiting periods can be very long, and options for care limited, and where the dignity and sacredness of life are reduced to valuing those lives based on costs and statistics.

this is just the tip of the iceberg’ the dems spent years writing this disaster. You don’t hear about all the qualifications and conditions it put on healthcare workers; wife is Surgical Tech, and it completely upended her employment. Obamacare is a disease all by itself.

When this act was passed during the Obama years, I blamed the dims. Then when republicans controlled both houses, the first two years of President Trumps, term, I blame the senator from AZ, John McCain. He let his hatred for the President, color his surely, better judgment. This act was a threat to “we th People”, IMOCongress needs to let the people buy their own insurance, like car insurance and homeowner insurance.

EVERYONE knew the ACA was a sham. Republicans [some] told the TRUTH at the time while DIMMs [ALL} lied about it! It was all a plan to eventually get to communist-style “health” care!

FACE IT – Obamacare is/was a Ponzi scheme just like Social Security.

It is very difficult to refer to ObamaCare as the “Affordable Care Act” when it is only affordable as a result of huge taxpayer subsidies.

Unfortunately, once the penalty for not purchasing health insurance was set at zero, it was inevitable that healthier people would just opt out.

Unlimited pockets cause this, just like college tuition. Also we think we should live forever and look good doing it.