Student loan payments have been due for six months now—yet no one seems to have told the students.

The federal government effectively suspended payments on student loans for four and a half years due to the COVID-19 pandemic, leading many borrowers to lose touch with their loan servicers and disengage from the repayment system. False promises of loan cancellation led to confusion and bitterness. As of October 2024, student loan payments are due again—but it should come as no surprise that less than half of borrowers are making them.

The Education Department hasn’t updated its official student loan repayment statistics since September. But Nelnet, the largest federal student loan servicer, provided me with data on the repayment statuses of the roughly 13 million borrower accounts they handle. The picture is dire.

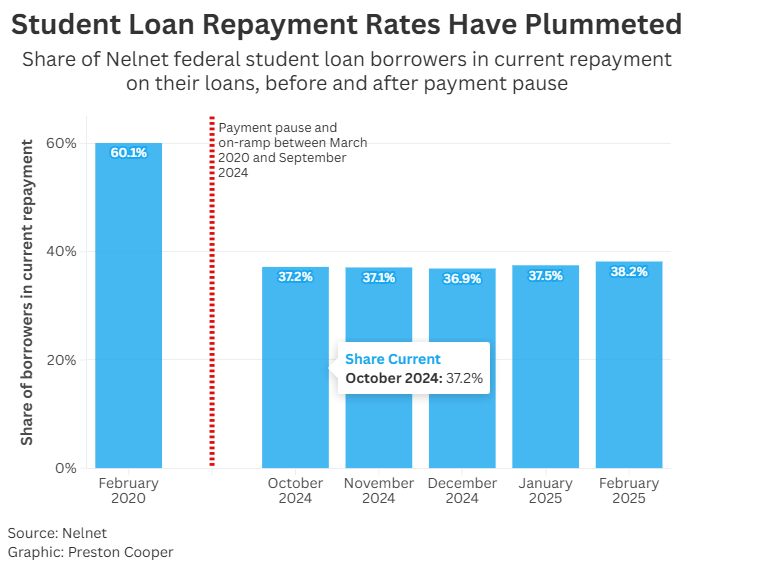

In February 2020, the last month before the payment suspension took effect, 60 percent of Nelnet’s borrowers were in current repayment on their loans. By February 2025, the share in current repayment had dropped to just 38 percent. Current repayment rates have not risen above 40 percent in the past five months since the payment pause effectively ended.

Around 20 percent of Nelnet’s borrowers are delinquent on their loan payments—a significant spike relative to pre-pandemic delinquency rates. Those delinquencies are now being reported to credit bureaus. Borrowers who continue failing to make their payments will eventually default, at which point they become subject to debt collection efforts such as the seizure of tax refunds and Social Security payments. “Without intervention, we anticipate the largest wave of defaults in the student loan program’s history—upwards of 3.5 million borrowers,” Nelnet says.

The other 42 percent of Nelnet borrowers are in deferment or forbearance. Many of these borrowers are enrolled in the Biden administration’s SAVE repayment plan, which is enjoined pending the outcome of legal challenges. The Education Department placed SAVE borrowers in forbearance while the challenges work their way through the courts. But the forbearance must eventually end when the court cases are resolved, leaving millions more borrowers at risk of delinquency and default.

Not only has student loan nonpayment spiked, but it now affects different types of borrowers. Student loan defaults were distressingly common pre-pandemic, but they mostly occurred among borrowers who already had a rocky credit record. Most pre-pandemic student loan defaulters had credit scores below 600, and they were roughly three times as likely as non-defaulters to be in collections on another debt, according to research by Kristin Blagg of the Urban Institute.

That has changed. Borrowers with good finances and sterling credit records, who could probably make their payments easily, have seen their loans fall delinquent. Many of these borrowers simply aren’t aware that payments are due again. Those with better credit have more to lose: data from Credit Karma shows that delinquent borrowers with the best credit records saw an average 137-point drop in their credit scores.

Spiking delinquencies should have been foreseeable. Four and a half years is a long time to go without making payments—borrowers move, stop paying attention to their loans, and lose contact with their servicers. The federal government has confused borrowers with conflicting and underwhelming messages about the return to repayment. The Biden administration made no real effort to alert borrowers about the end of the pause. The new Trump administration, meanwhile, has been distracted with other priorities.

The key to avoiding delinquencies is reestablishing contact with borrowers and clearly communicating their obligations to repay their loans and options to do so. But that takes resources—every call servicers place to borrowers demands an agent’s time, while every attempt to trace a missing borrower requires money—and Congress has appropriated no additional funds for the task.

A wave of delinquencies and defaults isn’t just a danger for borrowers—taxpayers are also at risk if loan repayments plummet. A 38 percent loan repayment rate, if it persists, is bad news for the Treasury. An administration and Congress focused on government efficiency may want to tackle the student loan nonpayment crisis before it is too late.

Preston Cooper is a senior fellow at the American Enterprise Institute (AEI), where his work focuses on higher education ROI, student loans, and higher education reform.

Reprinted with Permission from AEI.org – By Preston Cooper

The opinions expressed by columnists are their own and do not necessarily represent the views of AMAC or AMAC Action.

And why aren’t the lenders pursuing them to get payment? What’s really going on here? I know when I lost my job, I was mercilessly hounded to pay my student loan. These people had me such a wreck I didn’t know what to do. They didn’t give a damn that I had no job. I ended up selling everything I could and paid back every dime of my loan. Believe me, these people can pay, just as I did. Why are they being pursued for payment?

Is anything the government oversees a failure in the making? Student loans are one such example of default, the other was subprime housing loans. Irresponsible people really slap the faces of those that complete their financial obligations. It would appear that those student loans didn’t buy an education worthy of the debt they incurred. Reneging on student loans aren’t like people who just walked away from a car loan or mortgage, there isn’t anything to reposess. More importantly, irresponsible politicians defaulted on their obligations protect American taxpayers.

Stop making governments student loans! Let the school make the loan from their endowment slush fund. They will be more selective and the cost of going to college will probably come down. Might even lessen the over bloated staff at colleges and make the professors teach more classes.

Stop the student loans. You either pay or you go to a school you can afford. wipe out their credit records. Collect the money. These children need to learn responsibility. The taxpayers should not be made responsible for these spoiled brats. They do not repay the loans because they think someone else will pay for them. Many of them came no where near getting a degree. They have wasted hundreds of thousands of dollars. This would not have happened if parents had to cosign on these loans like it was previously set up. Putting the government in charge of anything immediately brings on disaster.

This brings the whole economy down. Taxpayers will owe more in taxes, the current borrowers will have lower credit scores keeping them from being able to buy larger items, and lenders will be less inclined to make student loans in the future. And probably also less likely to make loans period. Let me make it clear to the borrowers — you signed loan papers that clearly stated the lending institution would provide you money now and you would repay them at a certain rate over a specified period of time. The check is due!

Just another Democrat financial disaster. The 2020-24 borrowed money drug fest will haunt America for years. Thank you CCP

I vote for DOGE dismantling the federal government’s involvement in student loans.

No surprise, given the attitude of “entitlement” that exists and is growing in America. The degree of selfishness today is alarming. The average American feels no obligation to anything outside of “themselves”.

There has to be some hidden clause written in these federal student loans that is allowing the majority of these high amount student loans that allows such delinquency in any kind of repayment. I know that there’s a way to lower ( forgiveness of student loan debt) but it does mean a big ding on your personal credit just like a bankruptcy filing does. I feel that it is the overall use of bankruptcy filing as a debt cleansing without making the debtor personally responsible for the effect on the economy. The argument that tuition costs are higher today than in previous decades is merely an argument that works on paper in theory. What happened to acknowledging the extent of the debt loan which was made in a contract that the individual signed in agreement that states that there would be a pay back for the loan after achievement of the degree study. There was no qualifying provision for how to pay the debt like some of the excuses made —I don’t have that high paying expected job or I can’t find any job because I don’t want to work in any job unless it’s a job I want. Obviously, we have a large percentage of individuals who will only work if all job conditions are their version of ideal situation and they don’t have any other responsibilities of paying for necessity bills—rent/food/utilities—because they don’t pay for those things. And government benefit programs encourage people to not work enough to be self sufficient because the government benefits cover the necessity bills. There’s a bunch of protests going on this coming weekend ( first weekend of April 2025) concerning restrictions on removing these “benefits” from able-bodied people who feel deprived of their rights to live on dole paid by those of us who are taxpayers and don’t always have that dream job but we are earning our income and not getting any benefits unlike most of these protesters. They choose to get that expensive brand degree and knew the cost, yet don’t want to pay a dime for it. They can avoid paying by doing other forms of payment like community service for those communities that they feel should be helped—put their words into actions instead of protests.

No. The military has enough problems. It doesn’t need members who have both a sense of entitlement and a lack of duty/obligation to honor contracts and social constructs. There is no such thing as a free lunch, even less so in a military that can ill-afford to have people within it that believe it exists.

shysters, liars and thieves

It isn’t surprising that Federal and State governments have been living on borrowed money they do not expect to pay back until someone else has taken over the country.

3 years of mandatory military service would not be enough for most. Look at most of the liberals who might owe $200K+ so their service would have to be longer, but then again, the military quality would continue to suffer. Prison is out of the question as I would not like my tax dollars wasted. My Civil government teacher of the early 70’s had the best solution — put the delinquents on cleaning duty in their communities until their debts are paid for.

Exception: Service (military or equivalent civil) should be required before attending college. Higher education is not a requirement for a full life and so should be earned. The service first helps with the maturing process. We would see far less protest and far more academic success with older students attending college on their earned dime. Want proof? Look to the military service members who served, gained education benefits and attended higher education. They have an entirely different agenda in school and focus on more meaningful programs.

I’m not surprised by the failures of the Biden Administration to continue sending statements, invoicing and other messaging to continue informing borrowers of their loan repayment obligations. President Biden, himself, didn’t know he was, practically speaking, already deceased… which may have deepened the confusion of many borrowers… though he did seem to have a more orderly appearance than one would imagine in a mismanaged cadaver who was “resting in state” for an entire presidential term.

After graduating from college, I cut lawns and washed and waxed other people’s cars to pay my loan back in the mail 70’s. I wonder what percentage of these people who don’t pay commit themselves as such.

The government should not be in the business of student’s loans. If the parents are not well off enough, parents and kids should work together to pay for their education by saving and by the kids over 15 working summers and part-time jobs AND part-time while in college. The big reason schools get by with charging so much is because of the student loans. Your kid will appreciate his education more if HE/SHE has made a financial contribution for it. I raised 3 kids on my own and all of them are college grads and they all helped with the cost. Taught them a lot more than just what they were learning in college.

College is one of the biggest con’s in this nations history. Anyone who believes you need it… or you’re are destine for failure … HAS BEEN DUPED! Many wish they had never taken out the loans… even more that don’t even need the education for their current Job!

Payments would improve if the FED were not in the middle of the student loan boondoggle! The whole business drove up costs and waste at college level. Worse, these kids going to college are considered adult for the purpose of signing for student loans. No parental oversight but tax payers are essentially holding the paper.

What are the college majors of the students that do not pay back their loans?

I am 5 years old