The Trump administration’s ongoing work overhauling the federal student loan system reached a major milestone last month, when the Education Department published a proposed rule implementing key features of the One Big Beautiful Bill Act. The regulation’s impact analysis highlights key benefits of the Repayment Assistance Plan (RAP), a new loan repayment plan that will help student borrowers pay down their debts quickly and affordably—without mass federal loan forgiveness.

Currently, the federal government offers an array of income-driven repayment (IDR) plans, which tie student borrowers’ loan payments to their earnings and forgive remaining balances after a set period of time. The problem with these plans, as I’ve highlighted, is that income-contingent payments often don’t cover accrued interest—meaning borrowers who use them see their balances stagnate, or even increase, over time. This lengthens the time borrowers spend in repayment, meaning many see their loans forgiven outright after the repayment term expires.

RAP fixes this problem. According to the Education Department analysis, borrowers with typical levels of debt for undergraduates (between $25,000 and $50,000) will pay off their loans in just 12 years, on average. Compare this to other plans: under Income-Based Repayment (IBR), the main alternative to RAP, such borrowers would be in repayment for 15 years. The now-defunct SAVE plan, a creation of the Biden administration which slashed loan payments to zero for most borrowers, would have kept these borrowers in repayment for an average of 18 years.

Under RAP, Borrowers Pay Down Debts Faster

Estimated number of years in student loan repayment, by initial loan balance and repayment plan

As I recently explained in the Washington Post, RAP accomplishes this feat by waiving unpaid interest for borrowers whose income-contingent payments do not fully cover their interest. The plan also credits lower-income borrowers’ principal balances for each on-time payment. As a result, borrowers who keep up with their payments are guaranteed to pay down balances over time.

RAP pays for these new benefits by significantly paring back forgiveness. Under IBR, new borrowers can receive forgiveness after 20 years of payments. SAVE offered forgiveness after 10 to 25 years, depending on the initial loan balance. By contrast, RAP requires borrowers to make payments for 30 years before getting their loans forgiven.

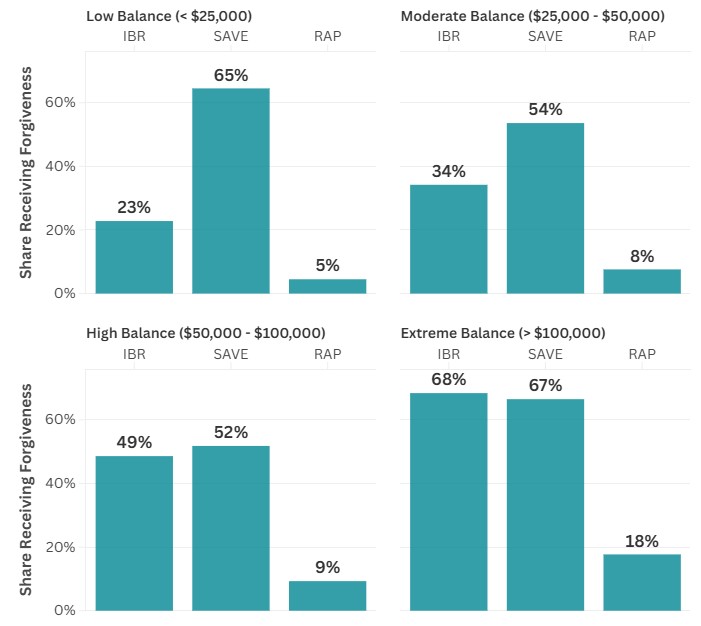

But because RAP borrowers pay down their balances so much faster, few wind up getting their loans forgiven outright. Just eight percent of borrowers with typical undergraduate debt will receive forgiveness under RAP, according to the Education Department analysis. Under IBR, around a third of typical borrowers could expect forgiveness, rising to two-thirds among borrowers with balances exceeding $100,000. Majorities of borrowers across the board could expect loan discharges under SAVE, making it more of a loan forgiveness plan than a loan repayment plan.

RAP Pares Back Loan Forgiveness

Share of borrowers expected to receive loan forgiveness, by initial loan balance and repayment plan

All this is good news for taxpayers as well. The changes to loan repayment plans will save the government around $368 billion through 2035, per the regulatory impact analysis. Even with the new interest waivers and principal credits, RAP borrowers will repay well over 90 percent of their original balances, even after accounting for the time value of money.

This dynamic will create a student loan system that is fair to both borrowers and taxpayers. While loan forgiveness is off the table for the great majority of borrowers—saving taxpayers hundreds of billions in the process—the Repayment Assistance Plan will also ensure that most borrowers escape their debt faster than they currently can. Advocates of loan cancellation like to say that student debt shouldn’t be a life sentence. The Trump administration is making sure it isn’t.

Preston Cooper is a senior fellow at the American Enterprise Institute (AEI), where his work focuses on higher education ROI, student loans, and higher education reform. Before joining AEI in his current role, Dr. Cooper was a senior fellow in higher education policy at the Foundation for Research on Equal Opportunity, a research analyst at the American Enterprise Institute, and a policy analyst at the Manhattan Institute for Policy Research.

Reprinted with Permission from AEI – By Preston Cooper

The opinions expressed by columnists are their own and do not necessarily represent the views of AMAC or AMAC Action.

1- if people are having such a hard time paying back student loans, is a college education really worth it?

2- Collages and universities that are worth hundreds of millions,if not billions of dollars shouldn’t receive one dime in taxpayer money via federal grants.

3- the reason tuitions are so high is because they know that the government is going to hand out student loans to pay for it. The federal government shouldn’t be loaning people money to go to school.

Of course, there is always the other way. Join the military come out and use your GI bill requirements or get a job and go to night school and have your employer help in paying for your tuition costs if you are getting an education in a degree that they accept would benefit their paying for.

Regardless of the payment plan my brother was duped into paying, thinkingit was the federal government. It must have been a scam.He never got any credit for what he paid.

So what’s next are we going offer this for their housing and buying a new car – where does the silver spoon end. It’s a loan, you signed for it in what we thought was in good faith to pay it back. You lied. You won. Congratulations, we’re all very proud of you.

Just another thing the government should not be involved in. We need to stop being the “Good ship lollipop” to all these dead beats and foreign nationals. I got an ADN, a BSN, and a MSN – no loans, no rich parents, no hand outs I did it by utilizing an amazing thing called work. And by the way, if the job you got with your student loan doesn’t pay the student loan you picked the wrong career field unless you’re studying poverty in America.

I have the parent plus loan now in IDR

i owe 145.000 can I apply for IFR